Until the Fed announced an expansion of its quantitative easing program two weeks ago, gold had begun to fade into relative obscurity. Sure, gold had risen in value from a low of $710/ounce back up to $900/ounce, but prices were still off 10% from the highs reached in 2008. Meanwhile, risk aversion had begun to decline and the stock market had begun to rise, such that pundits were talking more about stocks and less about gold.

Since the Fed’s announcement, however, gold has been thrust back into the spotlight. The same trading session that saw a record fall in the Dollar and a record rise in Treasury prices, also witnessed a 7% spike in gold futures prices. ” ‘Money is being pushed into the system and that’s creating the inflationary threats that the markets are contemplating…Commodities are a decent way to hedge against that potential threat,’ ” observed one trader.

Other analysts, however, caution that rising gold prices are a sign of the fear/crisis mentality, not inflation. “There are just not a lot of alternatives for global investors. You will see more and more investors moving into gold as a safe haven, and you will see more institutions putting money into commodities indexes.” In other words, gold is being driven by the safe-haven trade, which is evidenced by an increasing correlation with Treasury bonds. One commentator calls it a hedge against uncertainty: “The demand for gold is for gold coins, a massive flurry of bullion buying by ETF’s (and investors), and the institutions and traders buying the hell out of it. The reason is simple… pure fear.”

With the exception of the perennial gold bulls and conspiracy theorists, the short-term consensus is that due to “massive spare capacity now opening up in the global economy, soaring unemployment and a dysfunctional banking system – it would be very hard for central banks to generate a surge in inflation even if they wanted to.” This analyst further argues that the Fed is undertaking the expansionary program under the implicit assumption that it will have to siphon this money out of the financial system, if and when the economy recovers.

Of course, there is not even a consensus that gold is a good hedge against inflation. Mike Mish points out that the correlation between the US money supply and the price of gold is not very robust. When examined relative to a basket of currencies (rather than the Dollar), however, the relationship suddenly becomes much stronger. Especially when you filter out fluctuations in the value of the Dollar (which is affected by many factors unrelated to inflation), “gold is doing a reasonably good job of maintaining purchasing power parity on a worldwide basis.” This can be seen in the following chart:

Ascertaining a relationship ultimately depends on the time period of analysis, and the currency(s) in which prices are being tracked. Given also gold’s notorious volatility, it probably makes sense to use special inflation protected securities, rather than gold, as an inflation hedge.

ECB Prepares to Lower Rates, Euro Rally Fades

On Thursday, the European Central Bank will conduct its monthly monetary policy meeting. The consensus among analysts is that the meeting will lead to a 50 basis point cut, leaving the EU’s benchmark lending rate at 1%, a record low. Investors are also bracing for the ECB to announce certain unconventional steps, similar to the Fed’s program of quantitative easing, although not to such an extent. Analysts have speculated that the ECB “could intervene in bond markets to help ease companies’ financing problems.”

This marks an about-face from current policy and recent rhetoric, in which the ECB insisted that guarding against inflation was more important than providing economic stimulus. In fact, Jean-Claude Trichet, President of the ECB, has recently found himself on the defensive: “I don’t think it is justified to say we are doing less on this side of the Atlantic. We have automatic stabilizers,” he said during his quarterly testimony in front of European Parliament. In fact, the ECB had become an outcast among Central Banks for waiting a long time before finally agreeing to cut interest rates. Since embarking on a program of monetary easing, it has been playing catch-up by cutting rates at breakneck speed.

It appears that the ECB’s arm was twisted by the most recent economic data; a sudden drop in German manufacturing suggests that the recession is both spreading and deepening. Combined with a record drop in the EU economic sentiment, this “suggests that the euro zone economy will have contracted by roughly 2 percent quarter on quarter in the first three months of the year.” In addition, both producer and consumer prices have eased, such that inflation has fallen well below the 2% target level, and the ECB lost its last excuse for not dropping rates.

As a result both of the worsening economic situation, as well as the projected decline in yields, currency traders are once again questioning the Euro. The last couple weeks have been rife with commentary that the Dollar rally had come to an end as a result of the intensification of the Fed’s plan to use newly printed money to as a source of liquidity in the credit markets. “The dollar’s traditional trading patterns have been altered in the wake of new U.S. quantitative-easing measures. Risk appetite, stocks and funding currencies appear to hold lesser influence lately.”

This week, the narrative in forex markets favors the Dollar. It could be that the safe-haven trade has returned to lift the Greenback, but more likely is that investors are comparing economic fundamentals when making bets on currencies. One analyst summarized his firm’s position as follows: “We have argued that the leveraging-de-leveraging axis has been the key driver in the foreign exchange market. We expect a new driver, anticipated growth trajectories, to emerge…[and] for the dollar’s uptrend to resume in the second quarter.”

A Guide to Forex Leverage, and Employing it Safely

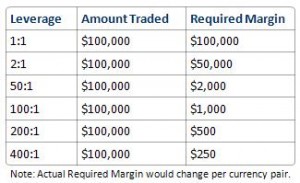

You have probably seen the advertisements - “Trade Forex with 400:1 Leverage” - without being entirely clear as to what exactly these brokers are offering and/or wondering why someone would want to leverage trades to such an extent.

Simply put, forex leverage (also referred to as margin) “is a loan that is provided to an investor by the broker that is handling his or her forex account.” With leverage, you can effectively increase your purchasing power, and buy securities in excess of what you would otherwise be able to afford, with the goal of maximizing relative returns. For example, if you achieve a 25% return on a $2000 trade/investment that was carried out with 2:1 leverage, you actually achieved a 50% return on the $1000 of capital that you personally invested; the other half, by implication, was provided in the form of a loan by the broker. Of course, the inverse also holds, such that a 25% loss would be magnified into a 50% loss, under the same parameters. See the table below for further understand this “multiplier effect.”

While traders can theoretically use margin to trade any kind of financial instrument/security, leverage is especially common in forex. The reason is that currencies are typically bought and sold in units of 50,000 - 100,000, which is more than retail traders can afford, or are willing to commit. Moreover, currencies are not as volatile (outside of the credit crisis, that is) as other securities, and typically don’t fluctuate more than 1% in a given day. Changes are often so minuscule that 1/10000 of a unit (one Pip) has become the benchmark for measuring fluctuations. Accordingly, “currency transactions must be carried out in big amounts, allowing these minute price movements to be translated into decent profits when magnified through the use of leverage.”

While traders can theoretically use margin to trade any kind of financial instrument/security, leverage is especially common in forex. The reason is that currencies are typically bought and sold in units of 50,000 - 100,000, which is more than retail traders can afford, or are willing to commit. Moreover, currencies are not as volatile (outside of the credit crisis, that is) as other securities, and typically don’t fluctuate more than 1% in a given day. Changes are often so minuscule that 1/10000 of a unit (one Pip) has become the benchmark for measuring fluctuations. Accordingly, “currency transactions must be carried out in big amounts, allowing these minute price movements to be translated into decent profits when magnified through the use of leverage.”

Leverage allows traders to put up only a fraction of the capital required to make a given-sized trade ; with 200:1 leverage, for example, $500 would be enough to fund a $100,000 trade. Unfortunately, leverage always favors the broker, much the same way that casinos benefit on average from extending credit to gamblers. According to one especially cynical commentator: “The game basically works this way: The broker is the shark. The retail trader is the shark food. If you want to make money currency trading, give yourself a fair chance and our advice is not to go more than 10x.”

A browsing of forex chat rooms and message boards reveals a surplus of disaster stories involving leverage, such that one can safely conclude that excessive leverage almost invariably leads to excessive losses. This lesson even seems to apply to institutional investors, despite the perception that they have an edge when trading forex, and hence would seem to represent excellent candidates for making leveraged trades. In the context of the current economic quagmire, “Investment banks were trading with 40:1 leverage in some cases. The banking crisis in the US was caused by banks not buying based on solid fundamentals and using insane leverage to buy securities.”

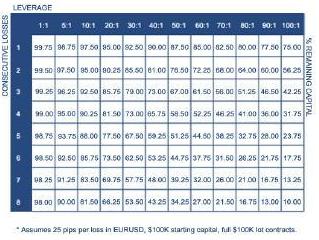

When trading a strategy that is based on technical analysis, “Even though you find one with 80-90% successful system on the paper, when you trade it usually come down 60%. So if we are losing at 40% of the time it is essential that we control risk.” Accordingly, putting more than 3% of your capital at risk on a given trade would seem suicidal. Applying more than 20:1 leverage (which seems trivial compared to 400:1) is very dangerous when you consider that a relatively benign 25 pip decline would result in a 5% loss. You can use the matrix below to calculate a “worst-case” scenario and figure out how much leverage you can get away with in the event that your trading strategy fails on consecutive occasions. It is surely much lower than you expected!

To give you an idea as to how excessive forex leverage has become, consider that the Financial Industry Regulatory Authority (FINRA) recently submitted a proposal that would prevent retail forex brokers from offering customers more than 1.5:1 leverage. While it’s possible that “The FINRA proposal sadly appeals to the lowest common denominator: the people who over-leverage positions with inappropriate stop-losses,” it nonetheless serves as a testament both to the danger of excessive leverage and to the importance of adequate risk management.

To give you an idea as to how excessive forex leverage has become, consider that the Financial Industry Regulatory Authority (FINRA) recently submitted a proposal that would prevent retail forex brokers from offering customers more than 1.5:1 leverage. While it’s possible that “The FINRA proposal sadly appeals to the lowest common denominator: the people who over-leverage positions with inappropriate stop-losses,” it nonetheless serves as a testament both to the danger of excessive leverage and to the importance of adequate risk management.

Pound Moves up Cautiously as Risk Aversion Declines

Since touching a fresh 24-year low in the beginning of March, the British Pound has recovered strongly, rising 5% against the USD in a matter of days. Analysts are at a loss to explain the sudden strength of the Pound, outside the confines of the safe-haven hypothesis: “The risk premium that sterling has taken on works both ways, and you can see sterling outperforming whenever risk appetite picks up.”

As another analyst points out, however, ascertaining the role of risk aversion in the markets has become somewhat circular: “Observers…draw this assessment purely from price action. Rising equities means the market is less risk averse. And the way we know there is less risk adversity is that the stocks have rallied.” Applying this argument to forex, softening risk aversion is contributing to a stronger Pound. At the same time, observers point to the rising Pound as a signal that risk aversion has softened. In short, the safe-haven trade is surely not the most convincing explanation.

In fact, by all accounts, the Pound should be falling. The latest data shows that retail sales plunged by 1.9% on a monthly basis. GDP is projected to fall to such an extent that “in 2009 Britain will slip to 12th place (from 7th in 2007) among the 15 ‘old’ members of the European Union, behind all except Spain, Greece and Portugal.” Meanwhile, the Central Bank of the UK has warned that Britain’s government finances have become so fragile that the government will have difficulty carrying out new spending plans. Investors have taken note, and demand for the latest auction of UK government bonds is believed to be the “lowest in history.”

Given all the bad news, perhaps the Pound’s recent rise can be best attributed to technical factors. “The $1.45 level represents so-called resistance on a descending trend line connecting the January high of $1.5373 and the February peak of $1.4986.” Given that the Pound has since sunk back below $1.45, it can be reasonably discerned that a cluster of sell orders were executed at this level.

Over the longer-term, the prognoses for the UK economy generally, and the Pound specifically, are not good. Thanks to a low exchange rate, inflation is actually rising. It is perhaps a welcome development, since it indicates that the UK was (temporarily) averted deflation, but it could also be a product of the quantitative easing plan announced earlier this month, whereby the Bank of England will flood the banking system with newly minted money. “Such a tactic can dilute the currency, and the perception that such dilution is about to occur is dragging the Pound down right now.”

Led by China, Central Banks Seek Alternative to Dollar

“China is a hostage. China is America’s bank and America basically says there’s nothing you can do to me. If I go down you don’t get paid.”

While the Obama administration has pledged the kind of fiscal responsibility that would secure its government obligations, its actions haven’t been so responsible. The Fed recently announced purchases of $1 Trillion in government debt, while the government is set to rack up Trillion-Dollar deficits over the next decade, even by the most conservative estimates.

In other words, China is in a quandary; stop lending to the US, and you might see the value of your existing reserves plummet. Continue lending, and you risk the same result. Tired of participating in this apparent no-win situation, China is finally taking action.

First, it will petition the G20 at its upcoming meeting for some level of protection on its $1 Trillion+ “investment” in the US. Meanwhile, Zhou XiaoChuan, governor of the Central Bank of China, has authored a paper calling for a decline in the role that individual currencies play in international trade and finance. According to Mr. Zhou, “Most nations concentrate their assets in those reserve currencies [Dollar, Euro, Yen], which exaggerates the size of flows and makes financial systems overall more volatile.” His point is well-taken, since of the $4.5 Trillion in global foreign exchange reserves that can be identified, perhaps 85% are accounted for by Euros and Dollars alone. When crises occur, everyone flocks to these currencies.

Mr. Zhou’s proposal is not without precedent. “His idea is to expand the use of ’special drawing rights,’ or SDRs — a kind of synthetic currency created by the IMF in the 1960s. Its value is determined by a basket of major currencies. Originally, the SDR was intended to serve as a shared currency for international reserves, though that aspect never really got off the ground.” It’s not clear exactly how such a system would work, but the idea is straightforward enough; instead of holding individual currencies, which are inherently volatile, Central Banks would be able to denominate reserves in a sort of universal currency. Instead of parking money in US Treasury securities, they would hold IMF bonds, or some equivalent.

Even before China starting becoming more vocal about its concerns, analysts had begun questioning the role of the US as reserve currency. I’m not just talking about the perennial pessimists. Within the context of the current credit crisis, a bubble may be forming in the market for Treasury bonds. “Foreign buying of American financial assets by both private investors and governments averaged $141 billion from September to December, Treasury data show…Demand was so strong that, for the first time, investors accepted rates below 0 percent on three-month Treasury bills to safeguard their capital.”

There is concern that a slight recovery in risk appetite (of which there is already evidence) could ignite a massive sell-off: “People are sitting there holding massive amounts of zero- yielding dollar assets. If there is any sort of good news, demand for dollars can drop off very, very quickly.”

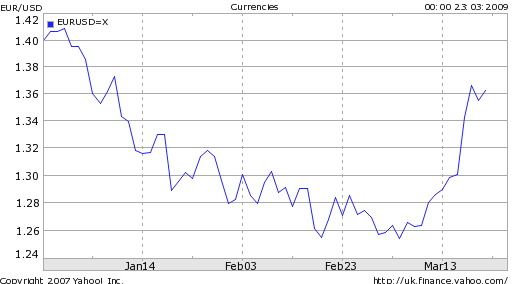

USD/EUR: Conflicting Signals Make Predictions Difficult

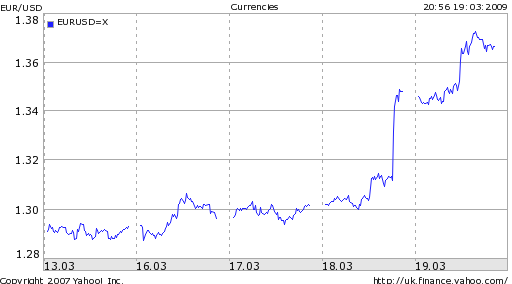

If you read analysts’ coverage of the Dollar decline (and consequent Euro rally), there is an even divide over whether it is sustainable. Economic data and technical indicators paint a nuanced picture, such that this kind of uncertainty is understandable.

On the one hand are the the Dollar bears, who point to an economic recession that continues to deepen, and the seeming complacency of the Federal Reserve Bank towards inflation. If there is any doubt as to how the forex markets feel about the Fed’s plan to purchase over $1 Trillion in US government bonds, consider that the the Dollar just recorded its worst weekly performance in 24 years, while the Euro simultaneously recorded its strongest week since its inception in 1999. There’s not much nuance there.

Meanwhile, the economic picture is equally depressing. Summarized by Kathy Lien of GFT Forex:

The Empire state manufacturing survey plunged to a record low in the month of March while Industrial production fell 1.4 percent, driving capacity utilization back to its record lows. Foreign investors reduced their holdings of U.S. assets by the largest amount since August 2007. Homebuilder confidence held near its record lows in the month of March as the slump in the real estate sector shows no signs of easing.

Unfortunately, there is a contradiction in the argument that the Dollar is being plagued both by economic collapse and by the risk of inflation. Writes Marc Chandler, head of FX strategy at Brown Brothers Harriman, “The pessimist camp wants it both ways. The US is going down the same path as Japan, where the end of a real estate bubble led to a banking crisis and a deep economic contraction. And they want to caution that printing of money will boost interest rates, fuel inflation and debase the currency.” He points out that history, as well as common sense, contradict this line of thinking.

Those that remain bullish on the Dollar argue that the Euro rally is a function of technical, rather than fundamental developments. First of all, we are approaching the end of a fiscal quarter. As evidenced by the Dollar decline which took place at the end of December, these periods are usually marked by portfolio rebalancing and hedging, such that it’s not uncommon to see large swings in forex markets. From a technical standpoint, when the Dollar failed to breach the $1.30 level against the Euro, many short sellers were probably forced to cover their positions, which accelerated the Dollar’s decline.

Bulls are confident that the pickup in risk-taking which catalyzed a 20% stock market rise is here to stay. “The move to the upside came after the government described a plan that will…generate $500 billion, and possibly $1 trillion over time, to buy hard-to-trade and badly deteriorated assets from banks.” The banks will be recapitalized, the financial system is being repaired, and everything will be okay, right?

The markets are certainly prone to false-starts. I can count numerous instances of government officials and market commentators insisting that “the worst is behind us.” Nevertheless, if this time proves to be different, it could be bearish for the Dollar, whose role as ’safe-haven’ currency would likely be eroded by a positive change in market sentiment.

Despite Shrinking Forex Reserves, China will Continue to Hold US Treasuries

Since Chinese Premier Wen Jiabao (as the ForexBlog reported here) expressed doubts about China’s US loans and investments two weeks ago, the markets have been awash in speculation. In hindsight, it seems that the announcement was a political ploy, rather than a harbinger for a policy change. With a few qualifications, therefore, it seems to safe to conclude that China’s foreign exchange reserves will not undergo any serious changes in the near-term.

Motivated both by politics and pragmatism, “China’s top foreign-exchange official said the nation will keep buying Treasuries and endorsed the dollar’s global role. Treasuries form ‘an important element of China’s investment strategy for its foreign-currency reserves,’ she said at a briefing in Beijing today. ‘We will continue this practice.’ ” The economic fortunes of China and the US have become increasingly intertwined over the last decade, such that China has come to depend on exports to the US to drive economic growth, while the US simultaneously depends on China to fund its fiscal and current account deficits. As a result, “about two-thirds of China’s nearly $2 trillion in reserves is parked in dollar assets, primarily U.S. government and other bonds.”

Even ignoring the potential political fallout from forex reserve diversification, such a move doesn’t really make practical sense. First of all, there isn’t a buyer sufficiently capitalized to relieve China of its US Treasury burden. “If China decided to sell off some of its U.S. Treasury holdings, it would scarcely be able to dump that in large blocks. And a partial selloff would surely lead to a slump in the Treasury market, eroding the remaining value of China’s portfolio.”

Even ignoring the potential political fallout from forex reserve diversification, such a move doesn’t really make practical sense. First of all, there isn’t a buyer sufficiently capitalized to relieve China of its US Treasury burden. “If China decided to sell off some of its U.S. Treasury holdings, it would scarcely be able to dump that in large blocks. And a partial selloff would surely lead to a slump in the Treasury market, eroding the remaining value of China’s portfolio.”

In addition, there doesn’t currently exist a viable alternative to US Treasury securities, nor to investing in the US, for that matter. China’s attempt at diversifying into corporate bonds and equities was extremely ill-timed, having been implemented just prior to the puncture of the real estate and stock market bubbles. Including the collapse in the value of its high-profile investments in the Blackstone Group and Morgan Stanley, total paper losses are estimated at a whopping $80 Billion. Investments in other currencies and markets, meanwhile, probably would have yielded similarly poor returns. The market for gold- mulled by some as a theoretical alternative- is even more volatile and “not large enough to absorb more than a small proportion of China’s reserves.”

As a result, China’s forex reserve diversification strategy is likely to proceed along two lines: change in duration of loans, and investments in natural resources. “The risk of short-term national debt is comparatively more controllable. China increased its holding of short-term US bonds by $40.4 billion, $56 billion, and $38 billion in September, October and November, respectively. At that time, China began to sell long-term government debt.” Through its affiliates meanwhile, China’s Central Bank is cautiously making stealthy forays into natural resources; see its recently-acquired a $20 Billion stake in Rio Tinto, an aluminum company, as evidence of this strategy.

Of course, China has announced tentative support for loaning money to the IMF and backing an ‘international’ reserve currency that would serve as an alternative to the Dollar. Given that this is probably many years away, however, it has little choice but to continue to hold Treasuries and the like. In the words of a high-ranking Chinese official: “We are in the middle of a crisis right now, and the priority for foreign exchange reserves is to minimize losses.”

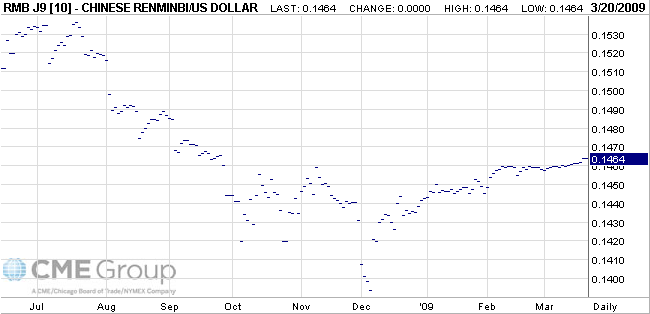

China Maintains “Stable” Yuan, at Least Against USD

China seems to have fulfilled its promise of a stable currency, given that the Yuan/Dollar exchange rate is one of the few bastions of stability in forex markets. One Dollar trades for approximately 6.83 CNY, about the same as it did last summer. Futures prices, meanwhile, reflect a mean expectation that one year from now, the exchange rate will dip only slightly, to 6.86 CNY/USD. [The inverse is depicted in the chart below].

In fact, there is even evidence that China is fighting market forces by trying to prop up the value of the Yuan. “‘ If this were a market-determined exchange rate, it would now be weakening, because the overall balance of payments looks to be in deficit, but it is not weakening,’ said [one economist]. ‘The implication is that authorities must be selling their dollar reserves in order to stabilise the USD-CNY exchange rate.’ ” Of course, it’s difficult to determine for sure, since the decline in China’s forex reserves that constitutes the basis for this claim could also have been caused by paper-losses on depreciating investments.

Within China, there is a core group of academics that continues to insist that China should depreciate its currency in response to deteriorating economic conditions. After all, China’s trade “surplus narrowed in February to $4.8 billion from about $40 billion in each of the previous three months, and in all likelihood will fall for the first time in five years in 2009.” Meanwhile, economists estimate that GDP growth could slow to 6%, a far cry from the 13% chalked up in 2007, and well below the government’s goal of 8%.

Some Chinese analysts also take issue with the notion of a ’stable’ currency. ” ‘The stability we expect is not only stability against the USD, but against all currencies,’ said MoC researcher Li Jian. ‘What is stability? Now the RMB is stable against the USD, but is appreciating against the euro, Australian dollar and the yen, so RMB’s exchange rates against these currencies are not stable.’ ” This is an important distinction, since China’s trade rivals are mostly nearby Asian countries- not the US. “Since July, the yuan is up 33% against the Korean won and up 12% against the Singapore dollar, for example. This has made Chinese exports relatively less competitive while spurring more imports and thereby providing somewhat of a boost to other economies.”

In the US, meanwhile, there are still policymakers that insist that the Yuan is undervalued, and the Treasury Department may brand China as a “currency manipulator” in its next semi-annual report. In the end, “with China holding its currency stable against the dollar even as its trade position has weakened, Washington’s long-standing argument that Beijing is keeping the yuan unjustifiably low is losing weight.”

Fed Turns on Printing Presses, Dollar Crashes

Having already lowered interest rates essentially to zero, the Fed has announced that it will now focus on ‘quantitative easing,’ a fancy way of saying that it intends to turn on the printing presses. It will purchase over $1 Trillion in credit instruments, split between Treasury securities and Mortgage-backed debt, expanding its balance sheet to $3 Trillion. This should (temporarily) put an end to speculation over whether foreign Central Banks are still willing to finance the US debt, as this question is now moot, since the Fed has demonstrated its willingness to fulfill that role. “The Fed is basically financing our deficit by buying the debt issued by the Treasury. If the Obama administration pushes through another stimulus package, the dollar is done.”

When the news was announced, the Dollar plummeted by 2.7%, the highest daily margin since 1971, as traders mulled the inflationary implications of printing over $1 Trillion and injecting it directly into the money supply, with the potential of more to come. Wrote one analyst, “Interest rates now are effectively negative across the board. The dollar is selling off because this may contribute to long-term weakness in the currency.”

Unfortunately for the Fed and the Dollar, the last few weeks have witnessed a slight pickup in risk tolerance, as investors began to focus more on fundamentals. If this development took place in the deepest chasm of the credit crisis, investors might have been willing to look the other way, but now they are very concerned that a huge expansion of the US monetary supply could trigger long-term inflation. A less pessimistic way of looking at the Dollar sell-off would be to attribute it to investor confidence that the Fed plan will help revive the global economy, decreasing the appeal of the US as a safe haven for investing.

Whether this will push the Dollar down further towards the $1.40 range depends on a couple factors. First of all, will other Central Banks follow suit? “All the major central banks may end up in the same position. The way we look to play it is to see which goes the first and which one lags, and try to explore the timing difference between the two,” explained one analyst. If this proves to be the case, investors will once again focus on the “least worst” currency, in which case the Dollar could once again come out on top.

It also depends on whether this action is intended as a quick fix, or as part of a series of purchases by the Fed. “Sell the dollar!” said…a portfolio manager. “This is huge, huge. It’s equivalent to the Plaza accord. This is the last thing theyhave in the closet, and they used it a bit early.”

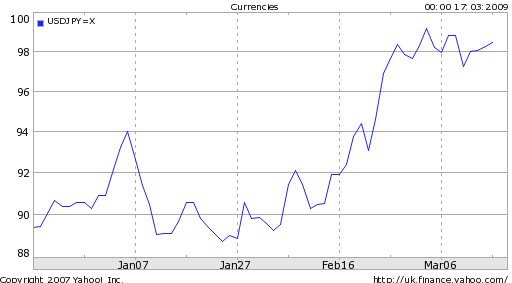

Japanese Yen Hovers around 100 JPY/USD, Intervention Unlikely

In the wake of the Swiss National Bank intervening to hold down the value of the Franc, everyone is wondering whether the Bank of Japan (and perhaps other Central Banks) will follow suit. Asks one market commentator rhetorically: “How long do you think it will be until Japan tries once again to push the yen lower, with its export industries in tatters?” Given that the Japanese economy is forecast to contract for at least the next two quarters, and also that its trade balance recently slipped into deficit, this is an eminently reasonable question.

Even prior to the surprise SNB announcement, it was widely speculated that the Bank of Japan would intervene on behalf of the Yen. After all, the BOJ was the most recent Central Bank to have waded into forex markets; it unsuccessfully spent $350 Billion in 2003-2004 to hold down the Yen. Since the inception of the credit crisis, however, it has passed on several golden opportunities. “It declined to intervene in October when the Group of Seven industrial powers issued a rare inter-meeting statement singling out yen volatility, giving Japanese authorities the green light to stem its surge. Even when the yen hit a 13 1/2-year high of 87.10 per dollar in January and exports demand collapsed, the BOJ held back.”

Since the beginning of 2009, the Yen has fallen 8% against the Dollar, and has fallen to a 3-month low against the Euro. Now, the “pendulum is swinging the other way” as risk aversion eases up and investors turn their attention to macroeconomic fundamentals. “The yen’s safe-haven appeal has, however, lost some of its lustre due to a rapid deterioration in Japan’s economy…and political uncertainty with an unpopular government facing an election that must be held by October.”

Nonetheless, the Yen has not yet slipped below the psychologically important 100 Yen/Dollar barrier. Analysts speculate that this is due to capital repatriation by Japanese investors, for hedging and accounting purposes. In order to minimize forex conversion losses, Japanese retail investors are taking advantage of the relatively weak Yen by shifting funds into domestic value stocks. Japanese companies, meanwhile, are ” ‘dressing up’ their balance sheets ahead of their fiscal year-end, by liquidating foreign holdings and bringing home the profits from overseas subsidiaries, to raise their bottom lines.”

The likelihood of BOJ intervention is paradoxical. If investors fear intervention, they will sell the Yen, and in turn, minimize the need for intervention. On the other hand, if investors remain skeptical of intervention, they may buy the Yen, which could actually impel the BOJ to intervene. But putting game theory aside, most analysts remain convinced that economic and political circumstances point away from intervention as a real possibility.

Swiss Bank Fulfills Promise of Forex Intervention, Franc Collapses

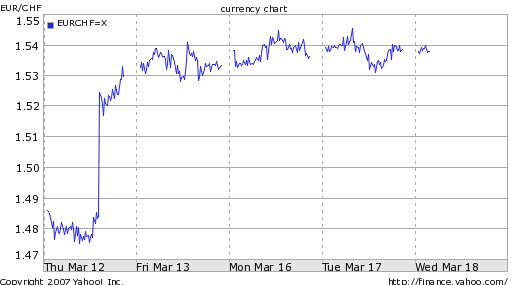

Last week, the Forex Blog concluded a post on the Swiss Franc by suggesting that the Swiss National Bank (SNB) could artificially depress the value of its currency, which had “not just posted strong gains against the euro since late August but has gained 8% on a trade weighted basis.”

The very next day, the SNB followed its widely anticipated rate cut by announcing that it would indeed intervene in forex markets, “implementing” a decision to buy foreign currencies. The Swiss Franc immediately fell into a tailspin, falling 7 units against the Euro, and more than 3 against the Dollar. According to one trader, “the way this was communicated was intended at maximizing its shock value.” By the end of the week, the Franc had posted a record decline, as investors remained alert to the possibility of further invention.

This is the first ’solo’ intervention since 1992 by the SNB, which has “followed a noninterventionist policy when it came to its currency, occasionally hinting at interventions but never following it up. It remained on the sidelines in September 2001 when the euro traded even lower than its present rate, at 1.44 Swiss francs.” It is also the first intervention by any Central Bank since 2003, when Japan intervened unsuccessfully to try to halt the rise of the Yen.

Evidently, the SNB felt justified in its decision not only because of a deteriorating economy, but more importantly because of monetary conditions. Inflation is now projected to dissappear by 2010, and may even “slow to the point where prices broadly fall.” Traders also speculated that the move was designed to relieve downward pressure on Eastern European economies, whose economic woes are being compounded by the fact that much of their debt is denominated in Swiss Francs.

It is doubtful that Switzerland will receive much sympathy from other countries, nearly all of whom have thus far refrained from forex intervention in spite of widespread economic contraction and the risk of deflation. In the words of one analyst, “It is troubling that a country with a current surplus larger than 10% of GDP feels compelled to depreciate its currency.”

The greater concern is that this could ignite some kind of “currency war,” where Central Banks around the world compete with each other to see who can most debase their respective currency. Traders are already speculating that the Bank of Japan could be next: “The BoJ should pay close attention to the SNB’s actions, given that both central banks have expressed a desire to see their currencies weaken.”

Korean Won Continues to Plummet as a Result of Acute Dollar Shortage

The Korean Won is among the biggest losers of the credit crisis, excluding Iceland of course. The currency has fallen 40% against the Dollar over the last year, even adjusting for a 10% rise in the last week. South Korean Finance Minister Yoon Jeung-hyun blames currency speculators, pledging that “The government will not sit idle when the foreign exchange rate is excessively tilted toward one direction or when there are speculative forces.”

Perhaps understanding that it cannot possibly hope to defend its currency against such a broad tide of determined speculators, the Central Bank of Korea has all but given up on intervening in forex markets. “South Korea was the catalyst for the shift away from defensive intervention. After spending 22 percent of foreign reserves from August to November to stem won losses, Yoon…said Feb. 25 that its weakness may be an ‘engine for export growth.’ ”

There is some plausibility to this argument, since South Korean economic fundamentals (as bleak as they are) probably don’t support such a precipitous decline in the Won. In fact some South Korean exporters have benefited from the weak currency, with companies such as Hyundai and Samsung growing revenues and increasing market share. Still, the global recession has impelled foreign consumers to cut back on spending, with the end result that “A double-digit fall in exports in the last three months of 2008 seriously undermined industrial production, [and] a 16% plunge in facility investment was an equally important factor in the 5.6% contraction in Korea’s GDP from the previous quarter.”

Ultimately, the Won’s decline is being driven by an acute shortage of Dollars. A relatively large portion of Korean public and private debt is denominated in foreign currency. The collapse in liquidity spurred by the credit crisis and consequent decline in bank lending have made it very difficult for South Korean borrowers to procure the requisite Dollars to repay their loans, causing a large imbalance in the supply and demand for the Dollar within Korea. Even more alarming is that $150 Billion of such debt will come due in the immediate future. “The government stresses that foreign debt maturing within a year amounts to 77% of its foreign exchange holdings, meaning Korea can cover its obligations. However, no other Asian nation that investors care about has such a high ratio of short-term external debt (on a remaining maturity basis) to foreign exchange reserves.”

South Korea recently extended a swap agreement with the US, which enables it to exchange up to $30 Billion in Won for Dollars. Investors are evidently hopeful that this represents a step towards easing the Dollar shortage, as the news caused the Won to appreciate by the largest margin in months. Borrowing costs for Korean firms remain high, and the odds remain tilted against them. Unless the US financial system stabilizes and/or Korea is able to run a current account surplus (as a result of increased foreign investment), liquidity will remain a problem.

Central Banks Maintain Holdings of US Treasury Securities, but For How Long?

Yesterday, Chinese Premier Wen Jiabao aired his country’s growing concerns about continuing to lend money to the US. Within the context of the US economic stimulus plan and other related US spending initiatives, Mr. Wen is understandably anxious about China’s vast holdings of US Treasury securities:

President Obama and his new government have adopted a series of measures to deal with the financial crisis. We have expectations as to the effects of these measures. We have lent a huge amount of money to the U.S. Of course we are concerned about the safety of our assets. To be honest, I am definitely a little worried.

While the announcement represented political posturing (to an increasingly restless, domestic Chinese audience), it should nonetheless be heeded as a warning, that the US cannot expect China (and other foreign Central Banks) to fund US budget deficits indefinitely.

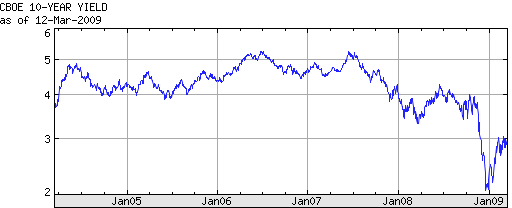

Let’s put aside the rhetoric for a moment, and examine the data. This week witnessed strong demand for Treasury securities, which were auctioned by the Treasury Department on consecutive days. Despite historically low yields (see chart), investors continue to snap up Treasury Bonds, mainly for the sake of risk aversion. The newly-revived issuance of 30-year bonds also went off without a hitch, and were more than 2x oversubscribed. Most relevant to this discussion is the fact the foreign Central Banks accounted for as much as 46% of demand!

The most recent Federal Reserve Statistical Release paints a similar picture. While foreign Central Banks and other international institutions reduced their holdings of US government securities slightly from the previous week, the decrease was essentially negligible. Overall, such entities have increased their holdings by at least $440 Billion over the previous year, bringing the total to approximately $3 Trillion (depending on the data source). China’s contribution remains substantial. Of its $2 Trillion in foreign exchange reserves, “Economists say half of that money has been invested in United States Treasury notes and other government-backed debt.”

However, there are a few reasons why I don’t think this trend will continue. First of all, the buildup in foreign Treasury holdings that transpired over the last decade was largely a product of unsustainable global economic imbalances, as net exporters to the US invested their perennial trade surpluses in what they perceived to be the world’s most secure investment. Temporarily putting aside whether Treasuries are actually secure, economic indicators suggest that Central Banks simply do not have the capacity to increase their holdings by much more. China’s trade surplus plummeted to $4.8 Billion last month; one economist projects a surplus of only $155 Billion in 2009, compared to nearly $300 Billion in 2008.

You can also remove from the list Japan- the second-largest holder of US Treasury securities- which is now running a trade deficit. Instead, both countries have publicly announced plans to use some of their forex reserves to fund domestic economic initiatives.

Then there is the equally unsustainable short-term buildup in US Treasuries, which is largely a product of technical factors. As I mentioned above- and which should be clear to all investors- the current theme underlying securities markets is one of risk aversion. In fact, it now appears that a bubble is forming in the bond market, and “any exodus now could spark selling across the board. Foreign debt holders would likely repatriate their funds immediately to reduce the risk of being last to convert.” As soon as markets recover- of which there are already nascent indications- investors will probably reduce their holdings of government bonds, or at least not increase their holdings.

Even the most conservative projections indicate a cumulative budget deficit for the next few years measuring in the the Trillions. Unless the risk-aversion theme obtains for the next decade, it seems unlikely that foreigners can be tapped to fund more than a small portion, leaving the Federal Reserve (with the help of its printing press) to make up the shortfall.

New Zealand Dollar (NZD) Benefits from “Deflation Trade”

2007 was the year of the carry trade. 2008 was the year of the safe haven trade. 2009, meanwhile, is shaping up to be the year of the deflation trade. In other words, traders have completed an about-face in their collective approach to forex, such that those currencies with the lowest rates are now favored, because they are perceived to best hedge against deflation.

The New Zealand Dollar illustrates this trend perfectly. For most of 2008, it collapsed as investors pulled money from risky, high-yielding currencies, in favor of a capital preservation strategy: accepting limited or zero return in exchange for security. Beginning at the tail-end of last year, however, it stabilized around the psychological level of .5 USD/NZD, failing to breach the important technical level of .4915.

While such technical factors undoubtedly have played a role in the reversal of fortune, the NZD has benefited by the aggressive interest rate cuts effected by the Bank of New Zealand, which today cut its benchmark rate yet again by 50 basis points, to 3%. While it’s too early to speculate whether the Central Bank will cut rates again at its next meeting, all signs point to further cuts. The economy is in a paltry state, having contracted for five consecutive quarters. Chinese demand for commodities is abating quickly, and the most recent numbers suggest it will continue to erode.

Based on investors’ current priorities, however, the most important indicator is the monetary situation, which appears under control. “The expectation that the RBNZ will be more moderate with cuts going ahead has provided support to the currency.” said…a currency strategist at Bank of New Zealand…“For a sustained bounce above 52 U.S. cents we’ll have to see an improvement in the global backdrop and evidence that equity markets have stopped falling and risk appetite is rebounding.”

Swiss Franc Rises on a Trade-weighted Basis, but Down against the Dollar

Most of the “safe haven” talk in forex circles has focused on Japan and the US. Switzerland, meanwhile, has also attracted is fair share of risk-averse investors, who are piling into Franc-denominated assets, despite the deteriorating Swiss economic situation. In fact, February witnessed an inflow of $4 Billion, most of which was targeted towards gold and money-market funds. The Swiss Franc, as a result, has appreciated by 9% (on a trade-weighted basis), since the summer.

The Swiss National Bank (SNB), meanwhile, has cut interest rates by 225 basis points over the last six months. If it delivers on a unanimously-anticipated 25 basis point cut at its meeting tomorrow, its benchmark lending rate will stand at a paltry .25%. To the frustration of the SNB, the “deflation trade” is still in vogue, as traders have counter-intuitively taken to betting on the countries and currencies that offer the lowest interest rates. From an economic standpoint, this trend is eroding the effectiveness of an easy monetary policy, such that the SNB has been forced to consider less conventional approaches.

This would probably take the form of quantitative easing, in the same vein as that which the US and UK are currently pursuing. Under such a policy, the SNB would buy credit instruments on the open market, and pay for them by printing money. This would have the dual effect of devaluing the Franc and easing liquidity problems in Swiss securities markets. While normally a country in Switzerland’s position (especially one whose banks have recently come under fire for secret bank accounts would take flak for such a policy, Swiss (economic) neutrality largely eliminates this burden. Another alternative, which has been proposed by the heir-apparent for SNB chief, is to create a ceiling on the value of the Franc.

Either way, a lower Franc looks like a real possibility. Says one analyst, “Switzerland is likely to…cut interest rates and intervened [sic] verbally to weaken the Swiss franc, threatening unsterilised intervention. If this does not work, and we are sceptical that it will, actual intervention may be required and we suspect this will have some impact. The bottom line is that the franc looks vulnerable.”

How to Develop and Backtest a Profitable Forex Trading Strategy

The holy grail of forex is a trading system that can turn a consistent profit, irrespective of the currencies involved and prevailing market conditions. While this has been promoted disingenuously by many a forex broker and forex software provider, suffice it to say that it remains elusive. A more realistic goal would be to build a strategy that is profitable most of the time (i.e. wins more than it loses). I don’t pretend to have developed such a strategy; instead, I would like to outline a method that can be used to confirm (or deny) whether your strategies are strong enough to withstand the daily whims of the forex markets: backtesting.

Simply put, backtesting involves applying a trading strategy to historical data. In other words, by checking the parameters that normally guide your trading against the way markets actually performed in the past, you can easily determine the stipulations/conditions that will make such parameters robust. Parameters include time period (hours, days, weeks, etc.), expected profit per trade (percentage, or number of pips), cumulative profit goal (i.e. 25% annual return) currency pair (USD/EUR, EUR/YEN, etc.) and comfort with risk (i.e. stop/loss). Stipulations, on the other hand, can be as simple or as complicated as you would like. For example, let’s say you want to buy whenever the currency pair breaches its 15-day moving average, and/or sell when the stochastic falls below a certain threshold. These kinds of stipulations can also be qualitative; let’s say, for example, you sell the Euro every time the European Central Bank lowers interest rates, or buy the Dollar every time the consumer confidence index records a rise.

The most robust strategies are profitable under a variety of market conditions, when profit goals are flexible. (For example, try adding or subtracting 5 pips to your expected profit per trade, and see if your strategy is still profitable). It is also important to remember that some strategies don’t lend themselves well to backtesting. Trendlines and other technical ‘patterns,’ for example, are often too circumstantial to be applied and tested generally. Backtesting also doesn’t account for market psyschology. While it would be nice to devise a strategy that is profitable in a variety of conditions, sometimes it must be condeded that when market sentiment is especially (and often irrationally) bullish or bearish, one’s strategy may not apply.

Having developed the paramaters and stipulations, how can you backtest your strategy? The pioneers (and perhaps even some stalwarts today) manually parsed reams of data, going through daily and weekly charts to determine the sets of conditions, if any, their strategies were viable. With the use of powerful computers, this tedious process can be completed automatically. If you’re not up for building/coding a system yourself, don’t despair, as there are a handful of great programs that have been professionally designed for amateurs to use.

Here, you have two main options. You can open a (demo) account with any of the forex brokers that incorporate backtesting software into their trading platforms. Pay special attention to those that use MetaTrader4 (MT4) - of which there are several reputable brokers- because it is the most critically-acclaimed and user-friendly. For those of you who don’t have access to such software, several downloadable versions can be found here, and a quick google search turned up a list of commercial software. Sometimes, such software requires you to provide your own historical data, which can be found here.

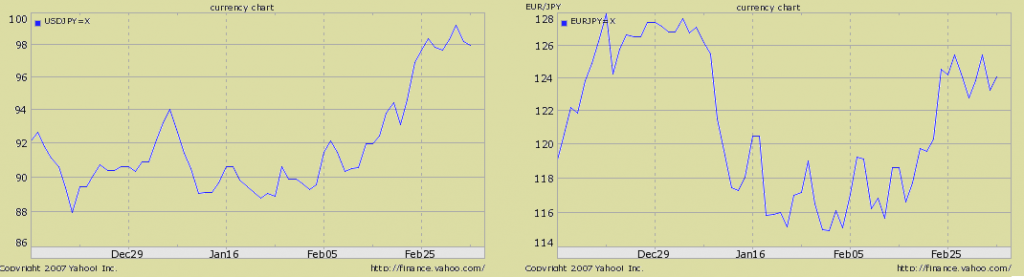

The Split Yen

The Japanese Yen is increasingly resembling a patient with split personality disorder, moving in one direction (down) against the Dollar while behaving quite differently against other currencies.

For most of the duration of the credit crisis, the Yen had mirrored the performance of the Dollar, both of which had performed well as so-called “safe-haven” currencies. For a while, the Yen even outpaced the Dollar, rising to a 13-year+ high. Over the last five weeks, however, the Yen has fallen off against the Greenback, while maintaining its value against other rivals. It’s unclear exactly what’s driving this split, but careful analysis suggests it is a product of changed investor psychology.

To elaborate, the Yen’s precipitous rise was due to financial- as opposed to economic- factors. As investors fled emerging markets en masse and unwound carry trades, it spurred a flood of capital back into Japan. This was not because the Yen was anything special; far from it, in fact. Rather, it was because the alternatives were perceived to be substantially more risky. This began to change in earnest when it was revealed that the Japanese economy shunk by over 12% (on an annualized basis) in the recent quarter. Given that Japan’s economy is famously dependent on exports, it didn’t take long for investors to connect Japan’s sagging GDP with its strong currency.

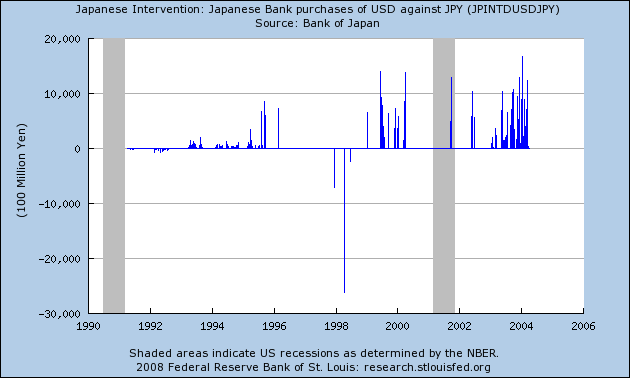

This prompted speculation that Japan would intervene in forex markets in order to prevent the Yen from rising further. In the end, Japan didn’t spend a dime. Fortunately, it didn’t have to, as investors took the hint, and sent the Yen tumbling against the Dollar. Technically, Japan hasn’t intervened since 2004 (see chart), but the threat of intervention combined with low interest rates ensured that in this case, words spoke just as loud as actions. It should be noted that Japan will use a small portion of its reserves to fund domestic economic initatives, but for now at least, none of it will be used to purchase Dollars in the spot market.

So why hasn’t the Yen reversed course against other currencies? Its stock market is sagging, and its economy is in equally bad, if not worse-than-average shape. The answer lies in interest rate differentials and investor risk tolerance. The rate gap between the Yen and the highest-yielding currency (New Zealand), has shrunk to less than 3.5%. Excluding Australia, and to a lesser extent the Euro, interest rate differentials are effectively negligible. Accordingly, investors have decided that the gains from an additional couple hundred basis points in yield are not offset by the perceived increase in risk associated with currency volatility. That this theory holds water is evidenced by the fall in the Japanese Yen that immediately registered when the Bank of Australia opted to hold rates steady at its most recent meeting.

UK, EU Central Banks Follow the Federal Reserve

Yesterday, both the European Central Bank (ECB) and the Bank of the UK cut their benchmark interest rates to record lows. This is especially incredible in the case of the UK, whose Central Bank over 300 years old! You can see from the following chart that both Central Banks have more than made up for their respectively slow starts in easing monetary policy by effecting several dramatic rate cuts, following the example of the Federal Reserve. The baseline UK rate now stands at .5%, only slightly higher than the Federal Funds rate, and slightly lower than the 1.5% ECB rate.

Given that they have essentially reached the terminus of their monetary policy options, all three Central Banks are exploring further options aimed at pumping money into their respective economies. The Fed has already “announced a program to buy $100 billion in the direct obligations of housing related government sponsored enterprises (GSEs) — Fannie Mae, Freddie Mac and the Federal Home Loan banks — and $500 billion in mortgage-based securities backed by Fannie Mae, Freddie Mac and Ginnie Mae.” As I wrote in a related article, “this was quickly followed by repurchase programs, lending facilities, investments in money market funds, and option agreements, all of which were designed to supplement its ‘traditional open market operations and securities lending to primary dealers.’ The Fed’s efforts also worked to ease the liquidity shortage in credit markets abroad by entering into swap agreements with several foreign Central Banks suffering from acute Dollar shortages.”

In conjunction with the rate cut, the Bank of the UK, meanwhile, will pump £150bn directly into UK credit markets through liquidity support, buying public and private debt, and asset purchases. “The main purpose of quantitative easing is not to send the money supply into orbit but to stop it from crashing…the broad money held by households has risen at a worryingly slow rate over the past year, and holdings by private non-financial firms have actually been dropping.” In contrast to the monetary programs of the UK and US, the ECB has thus far refrained from the kind of liquidity support that would necessitate printing new money. Instead, “the central bank will continue offering euro-zone banks unlimited loans at the central bank’s policy rate until at least the end of this year.”

The interest rate cuts were announced simultaneously with a spate of macroeconomic data, which collectively paint a bleak picture. Eurozone growth is projected at -2.7% for 2009 and 0% for 2010. The current unemployment rate at 8.2% and climbing. The thorn in the side of the EU is represented by eastern Europe, where growth is falling at an alarming pace, dragging the EU down with it. While EU member states have pledged to intervene if one of their own falls into bankruptcy, it’s unlikely that they would intervene similarly if a non-EU member state went bust. The UK economy is similarly desperate, having contracted at an annualized rate of 5.8% in the most recent quarter. The wild cards are the real estate and financial sectors, the fortunes of which are increasingly intertwined.

So what do the forex markets have to say about all this? Economists have used the dual phenomena of risk aversion and deflation to explain the interminable weakness in the the Pound and Euro. Everyone is surely familiar with the notion of the US as “safe haven” during periods of global financial instability. The deflation hypothesis, meanwhile, suggests that the ECB (and to a lesser extent, the Bank of UK), fell behind the curve when easing liquidity. The ECB, especially has harped on inflation as a reason for cutting rates more quickly. Given that investors are now more concerned with capital preservation than price inflation, it follows that they would prefer to invest where Central Banks were more vigilant about deflation (i.e. the US).

Personally, I think that the continued declines in both currencies, in spite of steep interest rate cuts, indicates that the deflation hypothesis is bunk, and investors remain fixated on risk aversion. By no coincidence, the temporary rebound in US stocks that took place in January was also accompanied by a bump in the Euro. (See chart below).

I think this mindset is reasonable, but only in the short-term. Given the current economic environment, I don’t think investors (and currency traders) can be faulted for ignoring the possibility that quantitative easing and liquidity programs will have to be funded with the printing of new money, which would be inherently inflationary. Many comparisons are being made with Japan, whose ill-fated quantitative-easing program succeeded only in inflating a bond-market bubble and vastly increasing Japanese public debt. According to one columnist, “it’s hard to argue that quantitative easing ended deflation; high oil prices did that. Meanwhile, the economy cured on its own most of the structural problems such as excess capacity and too much debt associated with the deflationary environment.”

In short, with a medium and long-term investing horizon in mind, I think the ECB’s approach to dealing with the credit crisis is more conducive to monetary stability. Thus, when investors grow weary of the idea of US as safe haven, they will no doubt focus instead on fundamentals. At which point, the ECB will likely be rewarded for fulfilling its anti-inflation mandate, in the form of a stronger Euro.

Forex Achieves New Prominence

Will Mexican Peso Crisis of 1994 repeat itself?

The main fly in the ointment was Mexico’s current account deficit, which ballooned from $6 billion in 1989 to $15 billion in 1991 and to more than $20 billion in 1992 and 1993. To some extent, the current account deficit was a favorable development, reflecting the capital inflow stimulated by Mexican policy reforms. However, the large size of the deficit led some observers to worry that the peso was becoming overvalued, a circumstance that could discourage exports, stimulate imports, and lead eventually to a crisis.

A sudden shift of funds out of a currency is called a speculative attack in the economics literature…Rather than waiting for the central bank’s reserves to run out through a gradual process of current account deficits, speculators who realize that a devaluation is inevitable will attack the currency through massive capital outflows as soon as they command enough resources to force a devaluation.

China Looking to Buy Oil & Diversify from US Treasuries

US Treasury yields have been held low across the short-term and long-term due in part to a lack of appealing investment opportunities in a deflationary period, while the Federal Reserve announced in January the possibility of buying long-term US government Treasury bonds to help hold down long-term interest rates (and thus mortgage rates), hoping for a slow controlled decent in housing prices.

At the other end of the spectrum, the US government has been bailing out every large financial institution willing to accept a few billion here or there, and running the printing presses in overdrive.

Eventually this will lead to inflation, as explained by John Williams last August:

Excess supply of a commodity or product usually is reflected in downside pressure on its price, and the same is true for money. Excessive supply of money leads to its debasement, to a decline in its value that otherwise is known as inflation. Where money supply generally is an underpinning of economic activity, it also is the ultimate determinant of prices and inflation. At present, near-record high annual growth in the broadest U.S. money measure M3 is suggesting a significant inflation problem in the year ahead.

The Chinese have nearly 2 trillion Dollars in their reserves, with roughly 2/3 of them being denominated in US Dollars. Seeing their own economy slow, and the coming risk of inflation, the Chinese government is looking to shift some of their reserves away from US Dollars to hard commodities, particularly oil. Marketwatch reports:

China is considering plans to tap its foreign reserves to buy crude oil as part of a push to diversify holdings from U.S. Treasurys, according to a published report.

With the U.S. issuing massive amounts of government bonds to finance economic stimulus measures, Chinese officials are looking to hedge against the risk of Treasury prices dropping.

China, which has been building up a national oil stockpile since 2004, aims to amass 100 million barrels by next year as a first step, the Japanese business daily Nikkei reported.

This may just be jawboning to try to slow down the US printing presses, but if it is more than that, it could have a significant effect on the perceived value of the US Dollar, especially in light of the current $1.75 trillion US deficit - a full 12.3% of the projected 2009 GDP. If foreigners lose confidence in the US Dollar, inflation and interest rates will certainly move sharply off their historic lows as the risk of “risk free” US treasuries is revealed and repriced.

Spike in Eastern Europe is Short-Lived

Growth in Poland, the biggest eastern European economy, will slow to 2 percent, the slackest pace since 2002, the European Commission forecasts. Latvia, a former Soviet republic, will contract 6.9 percent.

Fundamentals Catch up with Yen

A reversal of the yen, from strength to weakness, will have “major global implications…” Perhaps beleaguered Japanese authorities already have begun reacting to the “carnage” the yen’s rise has wrought.

Tidak ada komentar:

Posting Komentar